April 15, 2024

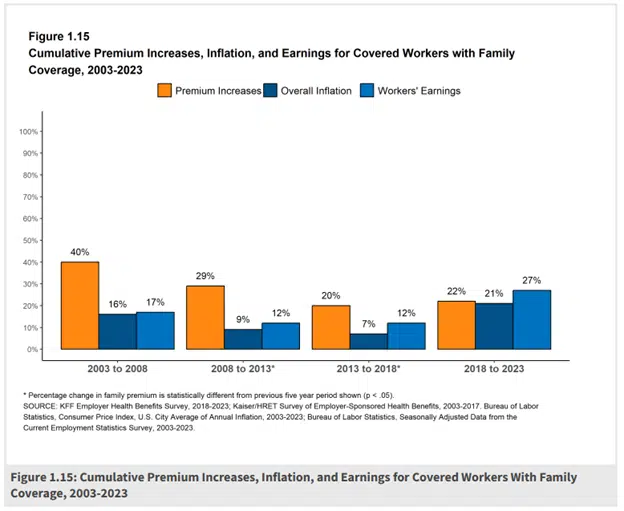

Over the last 10 years, the average annual health insurance premium outpaced inflation by 56% & worker wage growth by 11.90%.

Section 1: Cost of Health Insurance – 10240 | KFF

Which raises the question:

How can you attain health insurance affordably?

Considering that the U.S. on average spends almost double what the average comparable country spends per person – this question may cross your mind a time or two.

When it comes to health insurance there are a couple options to consider:

1. Public health insurance marketplace

The healthcare exchange acts as a matchmaker between insurers and individuals seeking coverage (Note: while purchase through government website, the government is not who you’re insurance is through).

This is the most popular option for many who don’t have employer provided insurance.

November 1st to January 15th is open enrollment for these plans unless you have a special enrollment opportunity (mainly getting married/divorced, having a child, turning age 26, loss of health coverage – in which you’ll have 60 days to choose new coverage). You can always evaluate what your coverage plans would look like through www.healthcare.gov/see-plans

When you evaluate plans you’ll be asked to enter your current plan, house size & income, age, and potential savings through the premium tax credit (more of this later). There will likely be hundreds of plans available so you’re going to want to filter your options.

Options to filter include:

- Desired monthly min/max premium

- Type of plan (catastrophic, bronze, silver, gold, platinum)

- Monthly premiums will be lowest for catastrophic & highest for platinum. The deductibles will be highest for catastrophic and lowest for platinum. Then your coinsurance (percentage your insurance company pays between your deductible and your max out of pocket) will be 60% for bronze, 70% for silver, 80% for gold, and 90% for platinum. Meaning, the remaining for the remaining percentage you will be on the hook for until your max out of pocket is met, then the insurance company will cover everything above that (note: the underlying coverage of these plans, if through the same insurance company is the same, the main difference is the monthly premium and how much you have to pay before the insurance kicks in)

- Max deductible

- Amount you will have to pay before insurance kicks in.

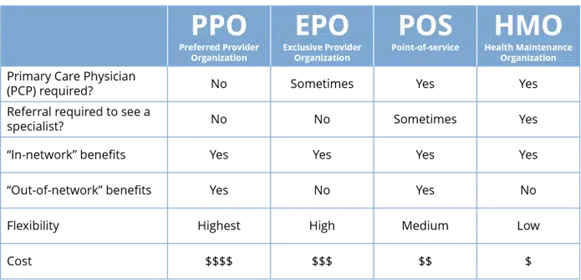

- Health plan type (PPO, EPO, POS, HMO)

- Whether a plan is Health Savings Account eligible

- Account you can save into pre-tax, funds can grow tax-deferred, and can be withdrawn free of tax for qualified medical expenses. You can read more about the tax advantages of your HSA HERE

- Specific plan, insurance companies, medical program, prescription drug needs, and medical providers.

- This is valuable if you’d like to keep certain medical doctors or to ensure your health insurance could cover your specific needs.

While there’s many personal considerations, the biggest medical plan consideration is going to be how much you spend on healthcare annually. A bronze plan may be a good fit for someone who rarely sees the doctor while a platinum plan may make more sense for someone with medical conditions requiring the frequent attention of a doctor.

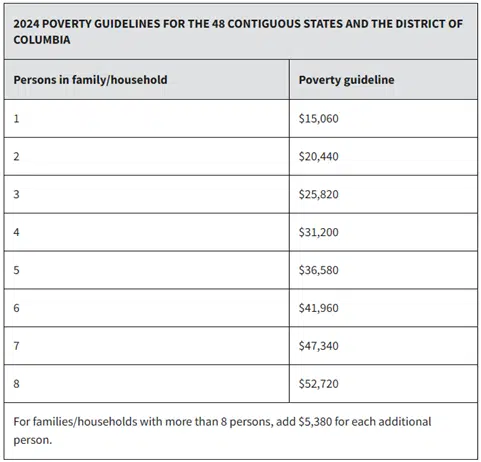

In terms of premium costs, if you have gross income that is 400% less than the federal poverty guidelines based on your family size, there may be a subsidy applied to your health insurance from the Premium Tax Credit.

If you’re a family of 4 and your gross income is below $124,800 ($31,200*4) then you’re eligible for a subsidy of your health insurance premium dollars (the credit is based on a sliding scale – greater for those with less income, less for those with high income until completely phased out). There are some planning strategies around keeping income low to qualify for the premium tax credit for the right individual who could qualify. Idea being:

If you can keep your income low enough, you can qualify for more of the credit & reduction in your monthly premium payment. Some options to consider would be:

- Pre-tax SEP/SIMPLE IRAs & 401k contributions

- Accelerating business expenses (if self-employed)

- Health Savings Account contributions

- Pulling income from high basis taxable brokerage accounts, cash value insurance policies, Roth accounts, or line of credit (SBLOC or HELOC)

Consider the following two plans (for a family of 4):

- My Blue Access PPO Platinum Plan:

- Premium = $3,796.60/mo

- Deductible = $0

- Out of pocket max (OOPM) = $10,000

- Coinsurance = 90/10 (you pay 10%, insurance pays 90% until your OOPM)

- My Blue Access PPO Bronze Plan:

- Premium = $2,035.14/mo

- Deductible = $17,800

- Out of pocket max = $17,800

- Coinsurance = 60/60 (you pay 40%, insurance pays 60% until your OOPM – for this plan, you’d be at your OOPM when your deductible is met)

Which plan is better for you?

Consider first, what are your health insurance costs?

Yes, this question is widely unknown. If you have a surgery, or need urgent care while on vacation, this would impact things – but on an average year, what do you typically pay? In the platinum plan, if you had $10,000 of medical expenses, you’d be on the hook for $1,000 and every dollar over $10,000 of cost would be paid for by your health insurance.

In the bronze plan, if you had $10,000 of medical expenses, you’d be on the hook for the full $10,000 because that’s part of your deductible. Until your deductible is met, co-insurance wouldn’t kick in.

But we’re missing on key thing:

With a platinum plan, you’re guaranteeing that you’re going to pay $45,559/yr in medical premiums.

With a bronze plan, you’re guaranteeing that you’re going to pay $24,421/yr in medical premiums.

The risk lies in your total healthcare costs.

If you have a catastrophic medical need year, the most you would have to pay in the bronze plan is $17,800. But even if you have $17,800 in medical expenses your total medical costs will be $42,221.

Compared to the platinum plan, you’re still better off by choosing the bronze plan by $4,337/yr maximizing both plans.

For the Bronze plan to equal the platinum plan, you’d have to incur $21,138 of medical expenses. Every year you don’t have more than $21,138 of medical expenses you get to pocket that difference as savings back in your pocket.

If you continue this for 10 years, that’s $211,380 of premium dollars saved. If you attach a 5% growth rate to those dollars, here’s what that looks like stretched over time:

- 5 years = $122,640

- 10 years = $279,165

- 15 years = $478,934

The trade off lies in the acceptance of uncertainty.

The higher deductible of the Bronze plan makes it less attractive than the Platinum plan which has a $0 deductible. To have to pay $17,800 before insurance kicks in can be a rough surprise but there’s a way you can prepare:

Having an emergency fund.

Keeping 3-6 months of savings in cash can help you weather a high medical expense year.

This is exactly what emergency funds are for – the unknown.

2. Health insurance through your current employer or continued coverage after your current employer health insurance (COBRA – or retiree health plan)

Consolidated Omnibus Budget Reconciliation Act (COBRA) allows you to keep the same coverage you had while you were still employed and typically lasts up to 18 months after a separation of employment (36 if the event is death, divorce, or the covered employee becomes entitled to Medicare).

If you look at your W2 box DD, this is your total employee plus employer cost of your health insurance. Typically, you’ll be required to pay this full amount up to 102% of the cost of the plan. This additional 2% charge is an administrative charge to keep your coverage as a non-employee.

If you have multiple years before Medicare eligibility, you’ll have to look at other options once COBRA runs out but keeping COBRA allows a more seamless continuation of coverage without having to go through the headache of picking a new plan.

3. Your spouse’s workplace plan (if applicable)

This is a great option if you cannot get health insurance through the open marketplace at a rate/coverage better than your spouse’s plan. You may find that some plans require a spouse to use their own health insurance if they have access to it through their employer.

4. You could get a part-time job that offers healthcare or join a professional association

The fundamentals here remain the same regarding whether this would make sense in the first place (premium, deductible, co-insurance, MOOP, etc.) but for someone who’s looking for a semi-retirement – this is a great option to consider.

5. Join a health sharing program

This is a type of plan where people pull their income together to cover the costs of other members.

This acts very similar to insurance – but is not actual insurance.

You pay an amount (similar to a premium), you’re then on the hook for a specified dollar amount (similar to a deductible), then need to pay a certain percentage of each service needed (similar to coinsurance) up to a max (like a max out of pocket). If you go this route, it’s important to consider what is covered and what is not per the health sharing agreement. Typically, these coverages aren’t as comprehensive health insurance on the open marketplace but generally are cheaper than traditional insurance. One popular health sharing program is Liberty HealthShare.

This could be a good option for someone who is healthier, higher income (not qualifying for the premium tax credit), and uses traditional healthcare minimally – if at all. But should be evaluated closely regarding what is/is not covered & stipulations on how their care network works.

6. Private insurance coverage (purchased directly through an insurance company or broker instead of the healthcare exchange)

It can be a hassle to do this on your own & your cost may be higher if you have pre-existing conditions (on the open marketplace, you cannot be discriminated against if you have pre-existing conditions).

7. Medicaid

Provided your income is 138% of the federal poverty line based on your family size – this is an option for you. Coverage will vary based on state.

8. Self-funded health insurance (not getting insurance at all)

The riskiest option of them all, not advisable, tread lightly here. Insurance is a transfer of risk. How much risk to transfer will be based on your coverage needs and desires – not everyone needs a gold or platinum plan to get great health coverage. In fact – that just might be an easy way to overpay tens of thousands of dollars a year.