July 15, 2022

The origination of stocks and bonds comes from a company’s desire to grow.

This desire to grow is constrained by a company’s cost of capital.

Or

The cost of obtaining money through issuing debt (bonds) or equity (stocks).

This is the rate of return that a company pays to investors who supply them money to grow.

Internally, a company optimizes how much debt or equity to issue based on their weighted average cost of capital (WACC).

Company’s like to issue stock because they don’t need to pay the money back.

But this comes at the cost of giving away the rights to future profits if the business is successful.

Company’s like to issue debt because they don’t give up rights to future profits (& interest is deductible).

But comes at the cost of having to pay back the loan in the future (with interest to debt holders).

As investors, we’re willing to lend a company money because we expect a positive return on our investment.

Whether that be from bonds, which are:

A loan from an investor to a business in exchange for a fixed series of interest payments over a specified period of time.

After the time period ends, the bond investor receives their money back.

For example, a company issues a $10,000 bond with 5% interest rate for 10 years.

An investor purchases the bond for $10,000 and over 10 years receives $500 in interest per year for 10 years. At the end of the 10-year period the company gives the investor their $10,000 back.

Or

Whether that be from stocks, which are:

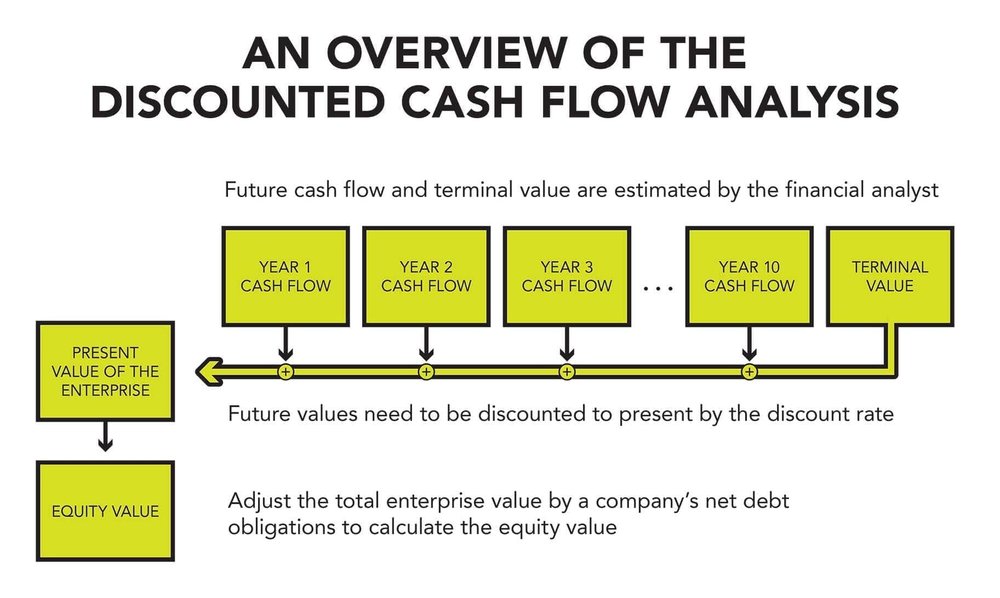

The present value of a company’s future discounted cash flows.

As a stockholder, you’re buying the right to a company’s future cash flows (or profits) discounted to the present.

You pay a price for the rights to those future earnings based on how risky the business is.

Those future cash flows are discounted to today’s pricing based on a combination of interest rates and the equity risk premium.

The equity risk premium = the increased discount you demand for the added risk of the uncertainty of a company’s expected future cash flow.

More stable and mature companies (Johnson & Johnson, Visa, etc.) = reduced discount rate applied

Less stable and young companies (Tesla, Airbnb, etc.) = higher discount rate applied

Issuing stock is a greater risk to investors than debt.

Why?

There is more uncertainty regarding expected return compared to fixed payments from bonds.

Stock prices fluctuate more frequently than bond prices, thus, increasing risk.

Stock realized returns reflect that as historically investors have been rewarded for this additional risk with higher returns.

A company’s realized equity return = expected return + unexpected return

Expected Return = the discounted rate the market applies to a company’s cash flows to reflect its risk

Unexpected return = the higher-than-expected cash flows generated from a company.

If a company does unexpectedly well, you will be rewarded with higher-than-expected returns.

For example, Tesla, Amazon, Google, Facebook (Meta), have had tremendous returns over the last 10 years.

Much of this excess return came from higher-than-expected profits.

It’s easy to lose all rational judgment when reading about a company’s sexy business model and superior growth potential.

Long term, unsexy profitable businesses yield higher returns than sexy unprofitable businesses.

If you flip a coin 100 times and you get 70 heads, are you more likely to believe you’ll get more heads over tails?

No.

Why?

Because you know that the probability of getting heads is 50%.

This is luck, not skill.

If you stretch out the number of coin flips and run 1,000 tests, you are likely to get a number around the average.

In the short run, there will be periods of time that produce results better than the average.

In the long run, the results come closer to matching the long-term average.

This is a concept known as mean reversion.

In capital markets, stock prices are mean reverting.

“Reversion to the mean is an iron law in stock investing”

— John C. Bogle, Founder of Vanguard

Stocks with high prices have historically led to lower realized returns.

Stocks with low prices have historically led to higher realized returns.

But stock prices don’t always go up.

Sharp market declines are a part of the stock investing (& should be expected).

Take Netflix, who recently reported first quarter earnings which revealed that the company lost 200,000 subscribers and that it expects to lose another 2,000,000 in the coming quarters.

The stock price plummeted from this and is down over 70% year-to-date.

Why?

Expected returns have fallen from decreased expected future cash flow.

As new information is divulged from quarterly and annual reports, stock prices quickly incorporate information into stock prices as billions of trades are made between buyers and sellers in an attempt to accurately reflect expectations of a company’s future profits.

But what about bond prices?

As a bond holder, your interest (or coupon payment) does not change regardless of a company’s expected future cash flow.

You can still expect to receive your interest payments and receive your money back at the end of the term.

Therefore, you don’t participate in the same volatility as stocks.

Bonds are composed of two core elements:

Coupon payment = interest payment from the issuing company

Yield to Maturity = total return on a bond if held until it matures

The key to note with bonds is:

Bond yields are inversely related to bond prices.

If interest rates increase, bond prices fall.

If interest rates decrease, bond prices rise.

Consider you buy a bond today issued at 4%.

If the Federal Reserve increases interest rates to 5%, are you willing to pay the same price for a bond paying 4% when newly issued bonds are paying 5%?

No.

So old bond issues paying 4% are discounted to make them competitive with bonds paying 5% (otherwise, no one would buy them).

This decreases your yield to maturity.

Conversely, if interest rates decrease during your bond term, your yield to maturity increases to reflect the fact investors will pay more to own a bond that pays a higher interest rate when comparably newly issued bonds are paying less.

Investors can use this phenomenon to dramatically reduce stock risk through the following:

- Avoiding stock picking

- Staying patient and disciplined

- Buying cheap and profitable companies

- Owning the total global stock and bond market

Companies will continue to issue debt and equity as they desire to grow.

As you invest, doing so informed allows you to become more steadfast amidst market volatility.

Don’t let current prices or fear of the unknown keep you from participating in human ingenuity.